Big news! "Paying for exports" will become history, and the new regulation will be officially implemented on October 1st!

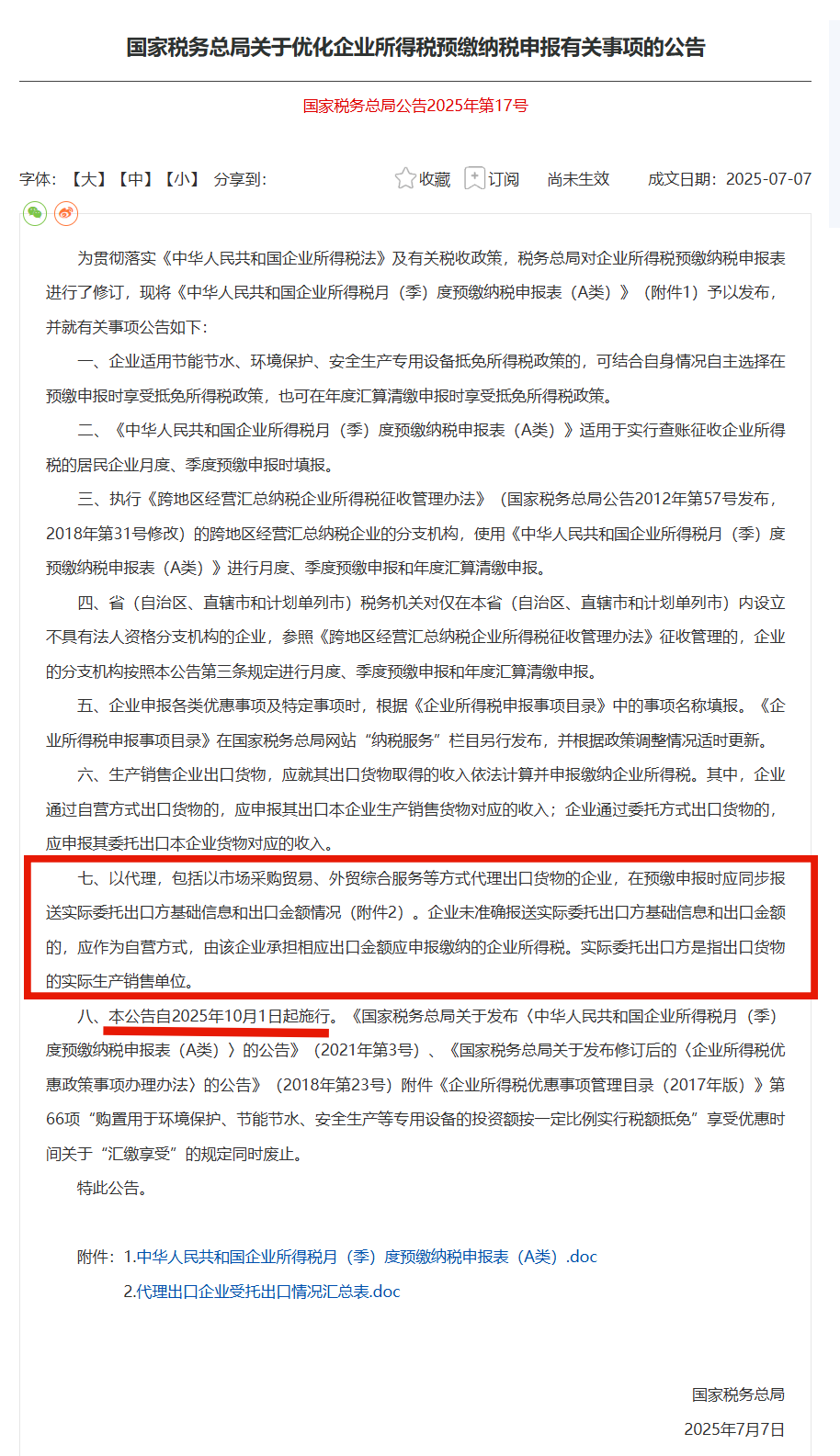

On July 7th, the State Taxation Administration issued the "Announcement on Optimizing the Declaration of Advance Payment of Enterprise Income Tax", which stipulates in Article 7 that enterprises acting as agents for export must report the information of the "actual entrusted exporter" and the export amount. Precisely crack down on the chaos of payment outlets.

The policy will come into effect on October 1, 2025.

I. Interpretation of Core Policy Points

1. Whoever sells goods pays taxes

? Self-operated export: production enterprises export by themselves ˇú Declare the income from export goods and pay enterprise income tax.

? entrusted export: Export by entrusting an agency enterprise ˇú the production enterprise still declares the income from goods and pays the enterprise income tax.

2. The agent must disclose the "true owner" of the export enterprise:

? declare income tax only on agency service fees

? mandatory submission for advance payment declaration:

? name of the actual consignor exporter

? taxpayer identification number/Unified social Credit code

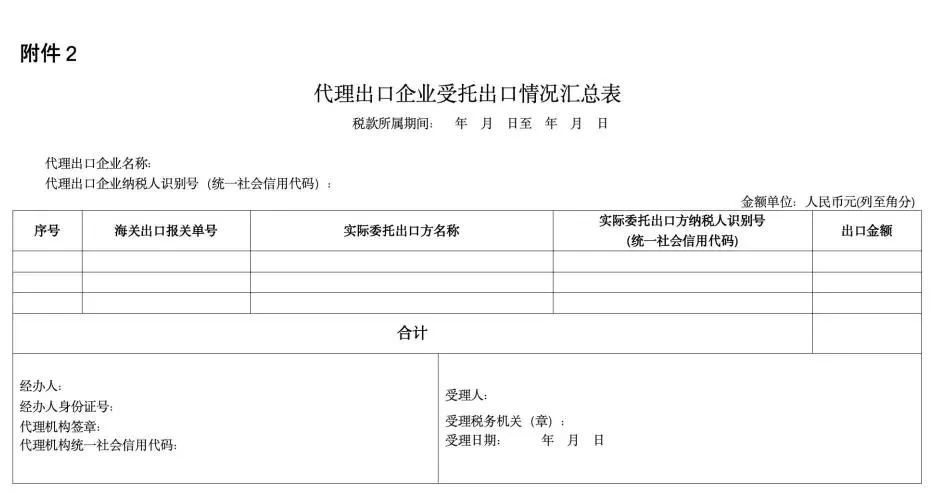

? corresponding export amount (with the "Summary Table of Entrusted Export by Export Agency Enterprises" attached)

Ii. Possible Impacts on Cross-border Sellers

Clear tax identity leads to a sharp increase in costs:

? Self-operated export positioning: The policy clearly states that purchasing and re-exporting is "self-operated" (Article 6), and the full amount of export sales (such as Amazon store income) should be included in the income and subject to enterprise income tax (25%), rather than only based on the profit. This directly dealt a blow to the tax avoidance models of "underreporting income" or "disguised agency".

2. Pressure on supply chain transparency

? Freight forwarder's reverse push: To protect itself, the freight forwarder will force the seller to provide the information of the real domestic supplier corresponding to the exported goods (including tax number) and the value of the goods. If the seller is unable to provide the goods, it may be rejected by the freight forwarder or regarded as "self-operated" (the seller itself needs to pay taxes according to the value of the goods).

? The end of "purchasing without invoices" : The model of relying on small suppliers that do not issue invoices is unsustainable. It is necessary to request and verify tax numbers from factories and integrate the supply chain.

3. Rising compliance costs

? needs to establish a supplier information database, match procurement costs with export sales, and upgrade the financial system.

? It is necessary to choose a compliant freight forwarder that can handle tax information reporting, and the cost may increase.

Iii. Enterprise Compliance Action Guide

? business authenticity is fundamental

The export goods must have actual buyers and traceable logistics tracks. The subsidy application materials and business documents must correspond one by one.

? Tax norms are at the core

Income must be fully declared, and corporate income tax, value-added tax and other taxes and fees must be paid in accordance with the law to avoid the double loss of "back taxes and fines".

? Prudent cooperation is guaranteed

When choosing service providers such as logistics and customs declaration, it is necessary to verify their qualifications to avoid being implicated due to their violations.